Highlights

“Capital markets posted gains in the 4th quarter, shaking off economic uncertainty, a rising inflation outlook, and higher import tariffs.“

Summary

Overall, the U.S. economy sent mixed signals in the 4th quarter of 2025, with weaker-than-expected GDP growth driven primarily by consumer spending and investment. While weak GDP growth was partially attributed to lower government spending amid the shutdown, the inflation outlook remained elevated, payroll growth remained sluggish and concentrated in a small number of sectors, and the housing market continued to show signs of weakening. Although the inflation outlook remained above the Federal Reserve Board’s target rate, the jobs market remained soft, leading the Federal Reserve Board to cut interest rates and signal a more cautious stance on future interest rate cuts.

Domestic production growth was positive in the quarter. An increase in consumer spending and investments contributed to GDP growth, partially offset by a decline in federal government spending.

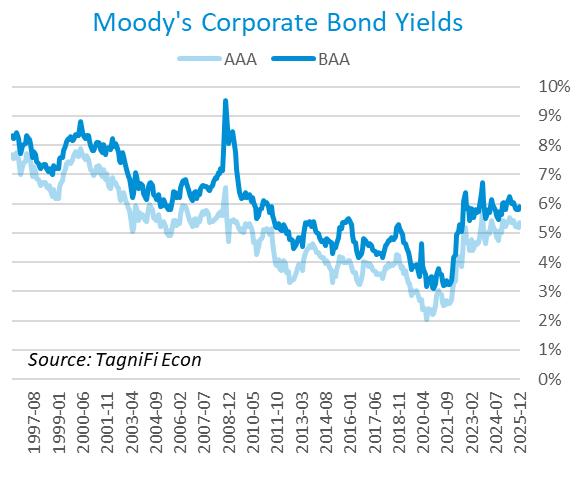

Inflation was in line with expectations despite higher prices in most categories compared to the previous quarter. Higher supply and concerns about softening U.S. and global economies led to lower crude oil prices. In response, the Federal Reserve cut the target interest rate and signaled that additional, albeit more moderate, rate cuts are likely in the coming months.

A frequent bright spot for the economy in recent years, the job market remained soft in the 4th quarter of 2025, with the unemployment rate steady, labor force participation slightly lower, and sluggish nonfarm employment growth. Still, the labor market remains well within the bounds of full employment.

Capital markets posted gains in the 4th quarter, shaking off economic uncertainty, a rising inflation outlook, and higher import tariffs. The tech-heavy NASDAQ indexes, broader S&P 500, and most Dow Jones Industrial indexes registered gains during the quarter. The Dow Jones Utility index declined during the quarter.

Housing market data continued showing signs of losing momentum, with slower price growth in several metro areas. As sales remained constrained by elevated interest rates, unsold housing inventory increased compared to the previous year. Still, prices in all four U.S. regions continued to rise year-over-year.

FOMC members’ short-term domestic production forecast was revised slightly upward, and the inflation outlook was revised slightly downward. The unemployment forecast was unchanged, while forecasts of longer-term economic performance were minimally revised.